Global ecommerce fraud losses exceeded $48 billion in 2025, according to Juniper Research, and they're projected to hit $107 billion by 2029. That number gets all the headlines. But the hidden cost is equally brutal: false declines from overly aggressive fraud rules block legitimate customers, costing merchants an estimated $443 billion per year (Aite-Novarica). Tighten fraud rules and you lose real customers. Loosen them and you lose money. AI fraud detection for ecommerce resolves this paradox by scoring risk in real time based on hundreds of behavioral signals, not rigid rules that treat every edge case as a threat.

This guide breaks down the five fraud types ecommerce brands face in 2026, explains why AI outperforms rule-based systems, and shows where AI-powered customer support fits into a modern fraud prevention stack.

Five Fraud Types Ecommerce Brands Face in 2026

Payment fraud remains the most visible threat. Fraudsters use stolen card data to place orders, often targeting high-value items with fast shipping. For every $1 of payment fraud, U.S. merchants lose $4.61 in total costs once you factor in chargebacks, fees, and operational overhead (LexisNexis). Friendly fraud, where the actual cardholder disputes a legitimate charge, now accounts for 36% of global fraud cases and drives chargeback volumes projected to hit 337 million by 2026.

Account takeover (ATO) is surging. ATO losses hit $17 billion in 2025, with 61% of all attacks targeting ecommerce (Sift). Attackers hijack existing customer accounts through credential stuffing, SIM swapping, and phishing, then use stored payment methods and shipping addresses to place fraudulent orders.

Return fraud costs U.S. retailers over $103 billion annually (NRF). Tactics include wardrobing (buying, wearing, returning), serial returning with intent to abuse, and empty box scams. One in five consumers admits to returning items after use. Learn more about how AI automates returns and refunds to catch these patterns early.

Promotional abuse drains margin through fake accounts exploiting new-customer discounts. Coupon fraud alone costs U.S. businesses over $600 million per year, and 73% of retailers worldwide report promo code abuse.

Synthetic identity fraud uses AI-generated fake customer profiles that pass traditional verification checks. Synthetic identity document fraud surged 311% between Q1 2024 and Q1 2025 (Sumsub), and up to 80% of new account fraud now involves synthetic identities.

Why AI Fraud Detection Outperforms Rule-Based Systems

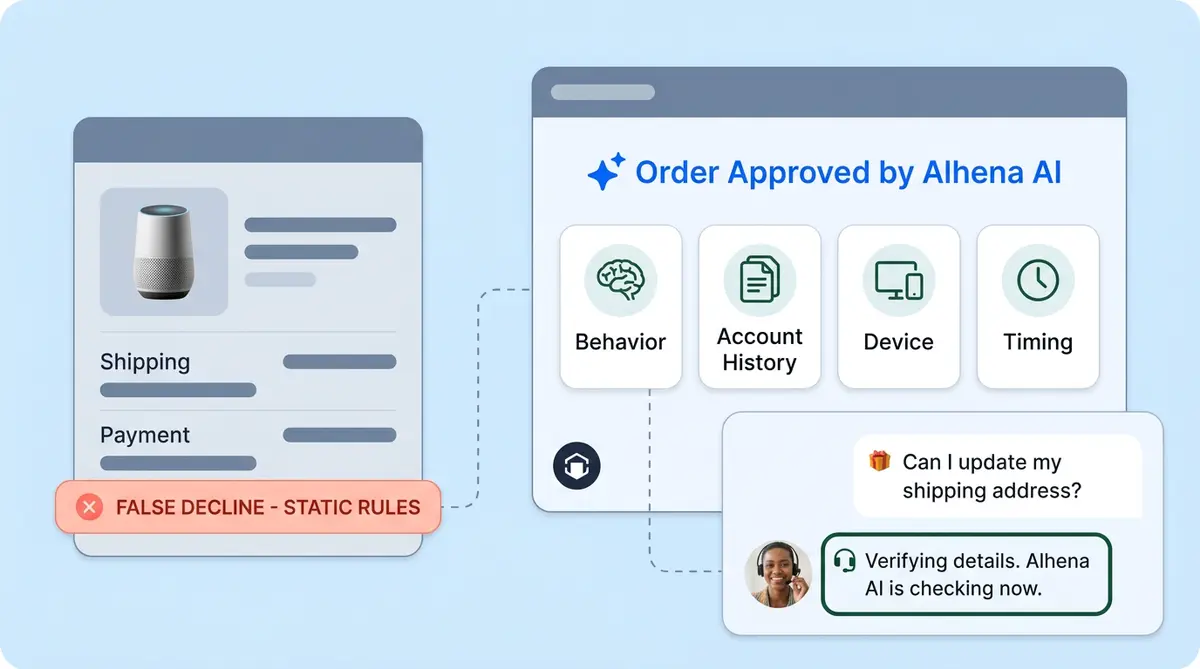

Rule-based systems follow static logic: flag any order over $500 from a new account, block transactions from certain regions, reject mismatched billing and shipping addresses. These rules catch obvious fraud but produce staggering false positive rates across millions of transactions. Danske Bank's legacy rule-based system had a 99.5% false positive rate before switching to machine learning.

AI systems evaluate behavioral biometrics, device fingerprinting, transaction pattern analysis, and network relationships simultaneously. These AI models and algorithms produce a risk score that adapts continuously as the system learns from millions of data points and transactions. The result: fewer false declines on legitimate high-value orders and faster detection of sophisticated fraud that static rules miss entirely. AI-powered fraud detection models analyze large datasets in real time, making split-second decisions with greater accuracy than any manual review process can achieve at scale. Mastercard reported a 300% improvement in detection rates after integrating generative AI into its fraud systems.

The False Decline Problem Nobody Measures

Sapio Research found that 33% of customers who experience a false decline never shop with that brand again. That means every wrongly blocked transaction carries lifetime value loss on top of the immediate lost sale.

AI-powered ecommerce fraud detection and prevention reduces false positives by learning individual customer patterns over time. A loyal customer placing an unusually large order from a new device gets approved because the AI recognizes their purchase history, browsing behavior, and account tenure. A rule-based system would flag and block the same transaction, losing both the sale and the buyer permanently. Better fraud detection data means fewer blocked transactions and lower risk of losing loyal shoppers.

Your Support Channel Is a Fraud Vector

Most ecommerce businesses treat fraud detection, fraud prevention, and customer support as separate systems. In practice, many fraud attempts flow through customer-facing channels. Forty percent of merchants don't monitor fraud for orders placed through contact centers (Ravelin).

Fraudsters chat or call to change shipping addresses on stolen-card orders after payment screening is complete. They social-engineer support agents into issuing unauthorized refunds. They request order modifications designed to redirect packages. Dark web "refund services" actively teach these techniques across underground forums, making refund fraud and chargeback fraud more accessible than ever.

An AI support agent trained to detect these patterns adds a fraud prevention layer that payment tools alone can't provide. The AI can verify customer identity through natural conversational challenges, flag suspicious order modification requests (shipping address changes on high-value orders placed within the last hour), detect scripted language patterns common in social engineering, and escalate suspicious interactions to a fraud review queue with full conversation context.

Where Alhena AI Fits in the Fraud Prevention Stack

Alhena AI isn't a payment fraud scoring tool. It's the AI-powered, customer-facing fraud detection layer that catches what payment systems and fraud detection software miss across channels. Here's how it works within a broader security stack:

Alhena's Order Management Agent verifies order authenticity by cross-referencing customer identity, order history, and request patterns before processing modifications. When a customer asks to change a shipping address on a recent high-value order, the agent checks account tenure, previous addresses, request timing, and risk data across recent transactions before executing the request.

The Support Concierge detects social engineering language patterns and escalates suspicious conversations to human review with full context. Instead of a human agent guessing whether a caller is legitimate, the AI flags behavioral anomalies and hands off a complete risk summary.

Alhena's integration with returns management tools flags serial returner patterns and wardrobing behavior, catching return fraud before refunds are processed. For brands using platforms like Narvar or ShipStation, this data flows directly into the conversation layer.

The hallucination-free architecture ensures the AI never provides information that could help a fraudster bypass security. Every response is grounded in verified account and order data, not generated guesses. A fraudster probing for account details or policy loopholes won't get useful answers.

Fraud Prevention Is a Customer Experience Problem

The brands that win don't just stop fraud. They stop ecommerce fraud without punishing legitimate buyers who drive revenue. That means combining payment-level fraud scoring with AI-powered customer support that catches social engineering, verifies modifications through natural conversation, and detects return abuse patterns.

Alhena AI sits at this intersection. It protects revenue on both sides of the equation: reducing direct fraud losses and chargeback risk through the support channel while preserving the buying experience for real customers who would otherwise get caught in aggressive fraud filters.

Ready to add a customer-facing fraud prevention layer to your stack? Book a demo with Alhena AI or start for free with 25 conversations.

Frequently Asked Questions

How does AI fraud detection reduce false declines without increasing fraud risk?

AI fraud detection evaluates hundreds of behavioral signals per transaction, including device fingerprinting, purchase history, and browsing patterns. Alhena AI adds a conversational verification layer that confirms customer identity through natural interaction rather than blocking the transaction outright. This dual approach catches sophisticated fraud while approving legitimate orders that rigid rules would flag.

Can AI customer support detect social engineering fraud attempts?

Yes. Alhena AI detects scripted language patterns, unusual request timing, and suspicious order modifications that signal social engineering. When a fraudster contacts support to change a shipping address on a high-value order, the AI flags the request based on account history and behavioral anomalies, then escalates to human review with full context instead of processing automatically.

How does AI detect return fraud patterns before refunds are processed?

Alhena AI cross-references return frequency, item categories, and customer behavior to identify serial returners and wardrobing patterns. By integrating with returns management tools like Narvar and ShipStation, the system flags suspicious return requests before refunds are issued, giving your team time to review instead of auto-approving every claim.

What costs more: false declines or actual ecommerce fraud?

False declines cost roughly nine times more than actual fraud. Ecommerce fraud losses total about $48 billion annually, while false declines cost merchants an estimated $443 billion per year (Aite-Novarica). Alhena AI helps on both sides by catching fraud through the support channel while reducing false positives that drive away legitimate buyers.

How does AI fraud prevention integrate with existing payment security tools?

AI fraud prevention works alongside your payment processor and fraud scoring tools, not as a replacement. Alhena AI operates at the customer interaction layer, catching threats that payment tools miss: social engineering through chat, suspicious order modifications, and return abuse patterns. Data flows between your payment stack and Alhena through secure API integrations.

What types of ecommerce fraud can AI detect that rule-based systems miss?

Rule-based systems miss synthetic identity fraud, sophisticated account takeover attempts, and social engineering through support channels. Alhena AI identifies these threats by analyzing behavioral patterns, conversational anomalies, and cross-channel signals that static rules cannot evaluate. The system adapts as new fraud tactics emerge rather than waiting for manual rule updates.

How quickly can ecommerce brands deploy AI fraud detection through customer support?

Alhena AI deploys in under 48 hours with no developer resources required. The platform integrates with your existing helpdesk (Zendesk, Gorgias, Freshdesk, and others) and ecommerce platform (Shopify, WooCommerce, Magento), so your customer-facing fraud prevention layer is active within days, not months.